Frequently Asked Questions

Do I need an estate plan?

If your answer to any of these questions is “yes,” you need to take the time to plan for your future and that of your family:

- Do you want to determine who will represent your interests after you’re gone?

- Do you want to decide for yourself how your assets will be distributed?

- Do you want to determine who will look after your minor children?

- Do you want to minimize or eliminate the time and expense of probate administration for your heirs?

- Do you want to minimize or eliminate estate taxes for your heirs?

- Do you want to help prevent conflicts among family members?

- Are you or your spouse a non-U.S. citizen?

- Do you have a blended family, with children (minor or adult) from a previous marriage?

- Do you want a portion of your assets to go to a charity or educational institution?

Why do people put off setting up an estate plan?

Most people would rather put off the topic of estate planning for another day…or another year. They say things like:

“I don’t want to spend the money right now.”

“It’s just easier not to think about it.”

“It’ll take care of itself.”

“It won’t be my problem.”

“I’ll live forever.”

“I know I need to do it; I’ll get around to it soon.”

“I don’t know how to start or who to talk to.”

It’s easy to put it off, but better to get it handled. The consultation is free and with no obligation. Get the advice you need and the help you deserve.

What happens when I don’t plan ahead?

When you don’t plan ahead by having a comprehensive estate plan:

- The Court appoints a guardian for you if you are incapacitated.

- Doctors and the Court make medical decisions for you if you are incapacitated.

- The Court appoints your personal representative upon your death.

- The Court appoints guardians for your minor children.

- Michigan law directs distribution of your estate to your “heirs at law”:

- Spouse.

- Children.

- Grandchildren, etc.

- If you have no spouse, your children receive your estate.

- If you have no spouse or children, your parents receive your estate.

- If you have no spouse, children or parents, your siblings, nieces and nephews receive your estate.

- If you have no spouse, children, parents, siblings, nieces or nephews (or descendents), your grandparents (or descendents) receive your estate.

- If you have no spouse, children, parents, siblings, nieces, nephews, grandparents, aunts, uncles or first cousins. . .

- The State of Michigan receives your estate.

By developing and implementing a comprehensive estate plan that includes a revocable living trust to hold and direct assets, you can help ensure your family can avoid the time, expense and hassle of Probate Court when the time comes.

What should a comprehensive estate plan include?

A comprehensive estate plan should include:

- Letter of Instruction—Letters of Instruction provide detailed instructions as to what final arrangements you desire, as well as other important information, such as the names of key advisors and financial service providers.

- Will—Your will names your family members, nominate guardians for minor children, and to direct any remaining probate assets (ideally, there won’t be any) to the trust for distribution under its terms.

- Funeral Representative Designation—A Funeral Representative Designation nominates someone to have final authority over making funeral arrangements.

- Revocable Living Trust—The Revocable Living Trust holds assets for distribution upon your death and to specify what those distributions will entail.

- Certificate of Trust—The Certificate of Trust provide basic information about the trust to financial institutions and title companies as needed.

- Basic Trust Funding Documents—Basic Trust Funding assigns or directs assets to the trust.

- General Power of Attorney—General Powers of Attorney allow your agent, generally trusted family or friend, to conduct business on your behalf while you are alive.

- Medical Power of Attorney—Medical Powers of Attorney allow your patient advocate to make decisions regarding your medical care if you are unable to participate in those decisions.

- Medical Records Release Power of Attorney—Medical Records Release Powers of Attorney allow your patient access to gain access to your medical records to assist them in making decisions regarding your medical care if you are unable to participate in those decisions.

- Advance Medical Care Directive—Advance Medical Care Directives allow you to specify what level of medical care you will receive.

How does Probate Court work?

The Probate Court oversees the distribution of a person’s assets when he or she dies with a will or without a will (called “intestate”). Once someone (a spouse, child, sibling or parent, for example) files an application to open a probate estate, the Court appoints a Personal Representative to collect assets, pay bills, and distribute the remaining property or money to those named in the will or, if there is no will, to that person’s “heirs at law.”

The probate administration process takes at least six months and can take much longer, depending upon the complexity of the estate and how well the heirs are getting along. The costs generally start at between $5000 and $7000 and can go up from there, again depending upon the estate and the people involved.

The Probate Court also oversees the appointment of guardians and conservators for minor children and incapacitated adults.

A good way to help ensure your family can avoid the time, expense and hassle of Probate Court is to develop and implement a comprehensive estate plan that includes a revocable living trust to hold and direct assets when the time comes.

How do trusts work?

A trust is a legal mechanism, not unlike a corporation or other legal entity, that can be used to hold property for later distribution to individuals and organizations. Unlike a will, which is a set of instructions for how to distribute assets, a trust is, in a sense, a “completed gift.” It names individuals or organizations as beneficiaries to receive trust assets.

Also unlike a will, a trust need not be administered or overseen by the Probate Court. It is a private document and generally results in a private distribution of assets.

When coupled with properly-drafted durable powers of attorney (financial, business, and health care), a trust can also provide guardian-like and consevator-like powers for the successor trustee (often an adult child of the trust creator) without the incuring the hassle and expense of petitioning the Court for these powers. These powers can help you manage and preserve parents’ assets to better provide for their care.

Do I really need a trust instead of just a will?

Gone are the days when only wealthy parents or grandparents set up “trust funds” for their children or grandchildren. Today, estates of even modest complexity generally should be placed into a trust for distribution. This generally includes deposit accounts, brokerage accounts, stocks, bonds, real estate, and life insurance proceeds.

This is especially true if there are minor children or an incapacitated adult. Whatever your situation, though, it’s important to meet with an experienced estate planning attorney who can help you determine the most effective and efficient way to transfer your property.

Why is a trust better than a will?

While not every estate fares better with a trust than with a will, it is often the case that a revocable living trust is a much better way to transfer assets than a will. Here’s why.

A will is a set of instructions that the Personal Representative (appointed by the Probate Court) uses to distribute assets to those named in the will to receive the estate (once all the bills have been paid, of course). The will is entered into probate; it’s part of the public record. The Court requires that notice of the death and of the probate process be published. The Court also requires that an inventory fee be paid to the court based on the value of the estate’s assets.

A trust, on the other hand, is a mechanism to transfer assets without going through the probate process. Unlike a will, a trust agreement is private. Publication of notice is not required (although there are situations when it’s still a good idea). There are no inventory fees due to the Court. Most important, though, is that a trust agreement is much more flexible, allowing you to defer distributions to beneficiaries, as well as to place certain conditions on those distributions.

Why do I need to “fund” my trust?

You fund your trust for the same reason you deposit money into your bank account: so the trust receives your property when you die. The trust language specifies how that property will be distributed. A trust without assets directed toward it is nothing more than a piece of paper (well, about twenty pieces of paper). We generally direct assets to the trust do this by naming the trust as an account beneficiary, perhaps behind living persons, such as a spouse and/or children. Assigning or directing assets to your trust takes those assets out of your estate, generally putting them beyond the reach of the Probate Court.

It’s important to understand that putting assets into a revocable living trust, a common estate planning tool, does not, by itself, protect those assets from creditors or from Medicaid “spend-down” requirements. These sorts of protections require more elaborate and carefully timed approaches to avoid Medicaid coverage disqualification or delay, as well as to avoid running afoul of the Court for concealing assets.

Should I place my tax-deferred retirement accounts into the trust?

It’s best to use beneficiary designations for IRAs and other tax-deferred accounts. This can allow survivors to keep at least some of those assets as tax-deferred for a longer time than if those accounts are distributed with other trust assets. However, it’s a good idea for the trust to be named as a contingent beneficiary after the other beneficiaries, to keep those accounts from being part of your estate and, therefore, subject to probate.

Should I put my home into the trust?

Generally, it’s a good idea to draft and record deeds to direct your home and other real estate to your revocable living trust. This is especially the case if you are not married. This way, your assets pass to your beneficiaries outside of the probate process, saving your beneficiaries substantial expense, including filing fees, notice fees, inventory fees and legal fees.

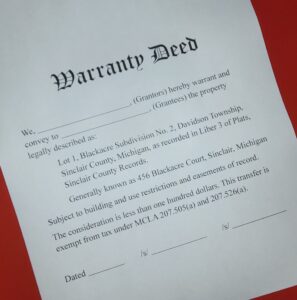

What kind of deed is best to use with my estate plan?

While many estate planning attorneys insist on using quit claim deeds with estate planning, I almost always recommend instead using a warranty deed, to direct real estate to a revocable living trust. A warranty deed helps preserve the protections afforded by the title insurance that you almost certainly paid for when you purchased the property.

Using a quit claim deed to move property into trust can have the unintended consequence of cutting off title insurance coverage, which will be catastrophic if, at some later time, issues arise with the property chain of ownership. Quit claim deeds, while appropriate in some specific cases, are not generally the proper way to handle your real estate when doing estate planning.

For some time now, I’ve been using an Enhanced Life Estate Deed (or so-called “Lady Bird” deed) when an estate plan includes real property. This type of deed allows you to maintain full ownerhip of the property in your own name, transferring the property to your trust only upon your death (or the death of a surviving spouse). This makes selling or gifting the property much easier than if it is in the trust. It also preserves the additional protections available to married couples with respect to their real estate. Note that these protections and the use of enhanced life estate deeds, while available in Michigan, may not be options for persons or property situated in other states.

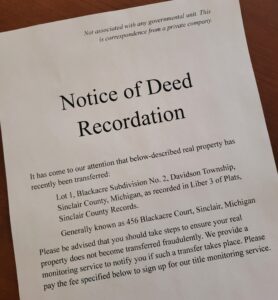

After I recorded the deed for my real property, I received an official-looking "notice" asking for additional fees. What should I do?

There are companies that go through public records and send solicitations offering “fraud notice” and other services for a pretty hefty fee. Most Michigan county Register of Deeds offices offer a similar service at no charge.

While it is of vital importance for you to protect the chain of title for your real property, it may not be necessary to pay a private company to help you with that. Visit your county’s Register of Deeds website and set up a title fraud alert.

How should I handle my interest in a closely-held business?

It is vital that you coordinate your estate plan with any business succession plan, which often means assigning your business interest to your revocable living trust. However, be aware that Federal law may require that your trust include special language, depending upon the type of business entity.

How should I handle my vehicles?

Generally, I recommend clients keep their vehicles in their own names, as Michigan law permits vehicles with an aggregate value under $100,000 to be transferred to an heir at law upon the owner’s death without involving probate court. When, however, the aggregate value of all vehicles exceeds $100,000 or if the transferee is not an heir at law, it may be advisable to transfer vehicles to a trust. Be advised, though, that such a transfer may be subject to state transfer tax based on the vehicle’s value.

Before you do this, be sure to consult with your insurance carrier first. Alternatively, you may want to execute a Transfer on Death document for each vehicle to name a “beneficiary,” allowing the vehicles to be distributed as you wish.

When a married couple owns multiple vehicles, I always recommend that only one name appear on a vehicle title and only the named owner of that vehicle drive it. This arrangement may help protect jointly-owned marital real property from legal action in the event of a serious accident or other money judgment.

Photo credit—This is a picture of our 1976 MG Midget. My wife, Krystal, and I, bought this car in 1980 from a guy who had almost certainly driven her through four Michigan winters. Her body was a mess, as was her top, but the tonneau cover, as far as I could tell, had never been used or even unfolded.

After about six years, I took “Midge” to a local body shop for the winter with the ask “Can you have her ready by spring?” This guy took her apart, right down to the to the frame, and rebuilt her from the ground up. Spring arrived and, with a color change to Brookland’s Green, new carpets, new interior trim, new rocker panels, a new floor panel, a new right-front quarter panel, a new wind screen, and a new top, she was absolutely primo.

Since then, we’ve put about 500 miles on her each summer, top down only, unless we get caught in serious rain. Huron River Drive, from Main Street in Ann Arbor to Dexter, is a great afternoon run. The Dexter A&W Drive-In still does car-hop service, a great throw-back to an earlier time, when life was, or at least seemed to be, a bit slower.

Will my estate be subject to estate tax?

Estates valued at or below $15 million face no Federal estate tax. For married couples, an estate tax sheltering plan can be crafted to shelter up to $30 million from estate tax. The amount above these exclusion levels is subject to a Federal estate tax of up to 40%.

Remember that your estate includes real property, life insurance proceeds from policies owned by you or your trust, and the value of tax-deferred retirement savings, such as IRAs, 401(k) accounts and 403(b) accounts.

How can I minimize the amount of estate tax my beneficiaries will have to pay?

When an estate exceeds the estate tax exclusion amount, a special trust mechanism can be established to shelter those assets from estate tax. Called a bypass trust (or A-B trust), this approach helps you reduce the amount of estate tax that will be due upon trust distribution. For very large estates, other mechanisms can be employed, such as irrevocable life insurance trusts (ILITs), non-taxable gifts to individuals (currently capped at $19,000 per gift), and tax-deductable gifts to one or more non-profit organizations.

It’s important to understand that proper trust planning, drafting and implementation can be complex and is essential. The difference between doing this properly and improperly can be hundreds of thousands of dollars (or more) in tax liability that could have been avoided.

What if I am or my spouse is resident non-U.S. citizen?

The estate tax rules are significantly different for non-U.S. citizens who inherit property. If a U.S. citizen inherits property from his or her non-citizen spouse, the unlimited marital exemption applies, and estate tax can be avoided. However, if a non-U.S. citizen spouse inherits, Federal estate tax must be paid on the entire inheritance.

Several approaches are available to help reduce or eliminate estate tax for such married couples:

- The U.S. citizen can make annual gifts of money or cash to his or her non-citizen spouse. The current limit for such an annual gift is just under $204,000.

- The non-citizen can apply for U.S. citizenship.

- A Qualified Domestic Trust (QDOT) can be established to receive the inheritance and hold it for the non-citizen beneficiary. The non-citizen beneficiary can then receive income from the trust for his or her lifetime.

How do I nominate a guardian and conservator for my minor child?

A good place to nominate a guardian and conservator for minor children is in your will. Your will is a legal document that has been signed and witnessed–it should be notarized as well. It has full legal force and effect.

Guardians and Conservators are appointed by the Probate Court. The Court generally looks favorably upon guardianship and conservatorship nominations. Judges, while always reserving the right (and having the duty) to act in the “best interests of the child,” usually give great deference to the express wishes of parents.

Can I nominate a guardian and conservator for myself?

Yes, you can. This is generally done as part of a Durable Power of Attorney (DPOA). In addition to delegating specified powers to another person (called the Agent), a well drafted DPOA also nominates someone (usually, the Agent) to serve as your guardian and conservator should you become incapacitated.

Guardians and Conservators are appointed by the Probate Court. The Court generally looks favorably upon guardianship and conservatorship nominations. Judges, while always reserving the right (and having the duty) to act in the “best interests of the protected person,” usually give great deference to an individual’s stated wishes.

Why do I need a medical power of attorney?

A Durable Medical Power of Attorney (MPOA) is an essential part of any serious, comprehensive estate plan. It provides a framework to allow someone else (called the Patient Advocate) to guide and manage your medical care if you are unable to participate in making those decisions.

The best medical POAs also provide guidance to your Patient Advocate as to the level of medical care you wish to receive in the form of an Advance Medical Directive (sometimes referred to as a “living will”). Providing an advance medical directive can help your Patient Advocate know what you want, making decisions a little easier at a time when they’re already difficult enough.

Should I have powers of attorney drafted for my college-bound kids?

Absolutely! Even though your kids are away at college, they may still need you to transact business on their behalf. A durable power of attorney for your children is almost a necessity.

Even more important is to obtain a medical power of attorney for your children, including the power to authorize release of medical records. Colleges and universities are bound by very strict regulations governing the release of medical information, even to parents. The only way to ensure that you can obtain medical records in an emergency is to have the proper durable powers of attorney drafted, executed and ready to use.

Can’t I just write my will and trust myself, or maybe go buy some software?

By all means, you certainly can write your own estate plan, just as you can repair your own car, replace your own roof, or even set your own broken arm. You may not save time, but you’ll probably save money, at least in the short run.

The trouble is that if there’s a problem, it might not surface until it’s too late. That’s when the value of having a professional becomes clear. Over the 25 years I’ve practiced law, I’ve seen several “homebrew” wills that, when the time came, failed to affect what the decedant likely wanted only because they had been drafted improperly.

The cost of an estate plan that is not done correctly can be huge when compared to the cost of working with an experienced attorney to make sure the job is done right the first time.

What about using online services to help me “write” my trust and will?

Sure, you can use these kinds of services to “draft” your trust and will–you’ll probably save some money, at least in the short term. Will you get everything you need? Will you take all the steps and check all the boxes? Will you actually get it all done, and done properly? Who knows?

It boils down to if, when you need help, you’re ok with calling “tech support” or trading messages with an AI bot. Perhaps instead, you’d prefer to have your work done and your questions answered by a real, live person—an attorney with 25 years of estate planning experience, not just a phone answerer or a data set programmed to guess the next word in the response. It’s your decision. Choose wisely.

How often should I review my estate plan with my attorney?

How often you should have your estate plan reviewed depends largely on where you are in life:

- In your 30s and 40s, every three to five years.

- In your 50s and 60s, every two to three years.

- In your 70s and above, every one to two years.

There are also life events that, when the occur, make it a good idea to contact your attorney to schedule an estate plan check-up:

- Marriage.

- Divorce (yours or a beneficiary of yours).

- Death of a spouse.

- A substantial change in the size of your estate (for example, if you receive a large inheritance or win the lottery).

- A move to another state.

- Death of any personal representative, trustee, agent, patient advocate, guardian, conservator or beneficiary you have named in your legal documents.

- Birth of adoption.

- Serious illness of a family member.

- Changes in any business interests you may have.

- Retirement.

- Change in your health.

- Change in your eligibility for life insurance.

- Acquisition of property located in another state.

- Changes in tax, property, probate, or trust law (if applicable to your estate).

- A change in your plans with respect to any of your personal representatives, successor trustees, agents, patient advocates, guardians, conservators or beneficiaries.

- Any new financial responsibilities.

How much is this going to cost?

Fees for estate planning are all over the map. There are attorneys who charge very low prices–and you’ll get what you pay for, but not necessarily what you really need. There are high-line law firms that charge very healthy fees for every meeting and every change–you won’t know the final cost until the project is finished.

Without sitting down and discussing your specific situation and needs, it’s difficult, if not impossible, to quote a fair and reasonable price for a proper estate plan, no matter what you’ve heard from other attorneys. However, know this:

- My fee to meet with you, listen to you, determine your needs, and make recommendations is zero. Our initial estate planning consultation is at no charge or obligation.

- My fee to draft your comprehensive estate plan is fixed, period. Once I understand what we need to accomplish, I can quote a fee that I’ll stand behind. You’ll know how much you’re spending before you commit to spending anything. This includes any and all meetings it takes to develop, review and complete your estate plan.

- While I need to make a living and pay my bills like everyone else, I strive to earn your business by offering the best possible value for the services I provide.

- Providing quality service for a fair price is paramount to me. I will never give “low-ball” price to get your business, then raise the price later. It’s just wrong.

- Finally, I will never ask you to “just trust me.” Instead, I’ll do what it takes to be earn your trust. The rest is up to you.